[ad_1]

Opposed choice is a basic drawback in medical insurance. For those who provide insurance coverage to people, you might wish to set the premiums primarily based on the common value of the inhabitants you propose to cowl. At this value, nonetheless, the sickest sufferers are those probably to take up insurance coverage and the well being insurer’s bills are more likely to be greater than anticipated. This may occasionally lead to an antagonistic choice loss of life spiral. One different is to mandate that every one people buy medical insurance, however authorities mandates are sometimes unpopular and the extent of protection that’s mandated additionally must be decided.

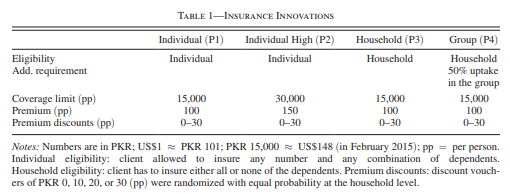

A paper by Fischer, Frölich, and Landmann (2023) goals to quantify the diploma of antagonistic choice in hospital insurance coverage for people in Pakistan. Pakistan has about 250 million people and annual per capita GDP is $5,200 (CIA World Factbook). To measure the quantity of antagonistic choice, the authors collaborated with the Nationwide Rural Help Programme of Pakistan (NRSP) to supply several types of insurance coverage to people throughout 83 totally different villages. Every village could possibly be provided particular person insurance coverage (P1) with a 15,000 PKR out-of-pocket most or a extra beneficiant particular person insurance coverage (P2) with a 30,000 PDR out-of-pocket most. Different villages have been assigned to family insurance coverage (P3) the place all people within the family are required to enroll within the insurance coverage and a “Group coverage” the place >50% of a credit score group or group organizations (COs) are required to enroll within the insurance coverage. The desk under summarizes these choices.

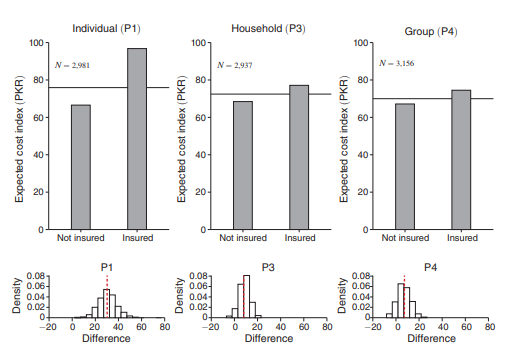

Utilizing this method, the authors discover that there was:

…substantial choice in particular person insurance policies, resulting in welfare losses and the specter of a market breakdown. Bundling insurance coverage insurance policies on the family degree or greater virtually eliminates antagonistic choice, thus mitigating its welfare penalties and facilitating sustainable insurance coverage provide

One can clearly see this outcome from the determine under. One vital level to notice is that common family dimension within the experiment was 5.99. Thus, it’s unclear if antagonistic choice can be mitigated to the identical diploma in higher-income nations the place family dimension is smaller.

The total article is on the market right here.

[ad_2]

Source link